There is a persistent and expensive misconception in mining project development. It is the belief that a completed Bankable Feasibility Study is the primary document a lender needs to issue a mandate.

It is not. A BFS is one input into a much broader evaluation process. And the dimensions that a lender's credit committee weighs most heavily at the pre-mandate stage are precisely the ones that a BFS is not designed to address.

Understanding what lenders actually evaluate — and why the BFS leaves three of the five critical dimensions largely unanswered — is the single most important thing a developer can know before approaching a bank.

Five Dimensions. One Credit Decision.

Every project finance lender evaluates a mining project across five dimensions before issuing a mandate. These are not theoretical categories. They are the structured assessment framework that a credit committee works through, and every material deficiency across any one of them can prevent a mandate from being issued regardless of the strength of the others.

- Technical. The geological confidence of the reserve base, the reliability of the process design, the realism of the mining sequence, and the adequacy of the capital cost estimate. This is the dimension the BFS addresses most directly.

- Financial. The quality and lender-readiness of the financial model, the adequacy of the funding structure, the DSCR under stress scenarios, and whether the model has been built to bank conventions or the developer's own assumptions.

- Environmental. The permitting pathway and status, the quality of the Environmental and Social Impact Assessment, the tailings governance framework, climate risk exposure, and closure planning.

- Social. The social licence to operate, the quality of community engagement and consultation, resettlement obligations, indigenous peoples' rights, and the labour and human rights framework.

- Governance. Corporate governance quality, beneficial ownership transparency, anti-bribery and corruption compliance, jurisdiction and political risk, and the track record of the management team.

A BFS addresses Technical comprehensively and Financial partially. Environmental, Social, and Governance are addressed minimally, inconsistently, or not at all.

The credit committee does not evaluate these dimensions sequentially. It evaluates them simultaneously. A project with outstanding technical credentials and an unresolved social licence question does not receive a conditional mandate pending resolution of the social issue. It receives no mandate until the social issue is resolved. The five dimensions are a threshold, not a weighted average.

What the BFS Covers Well

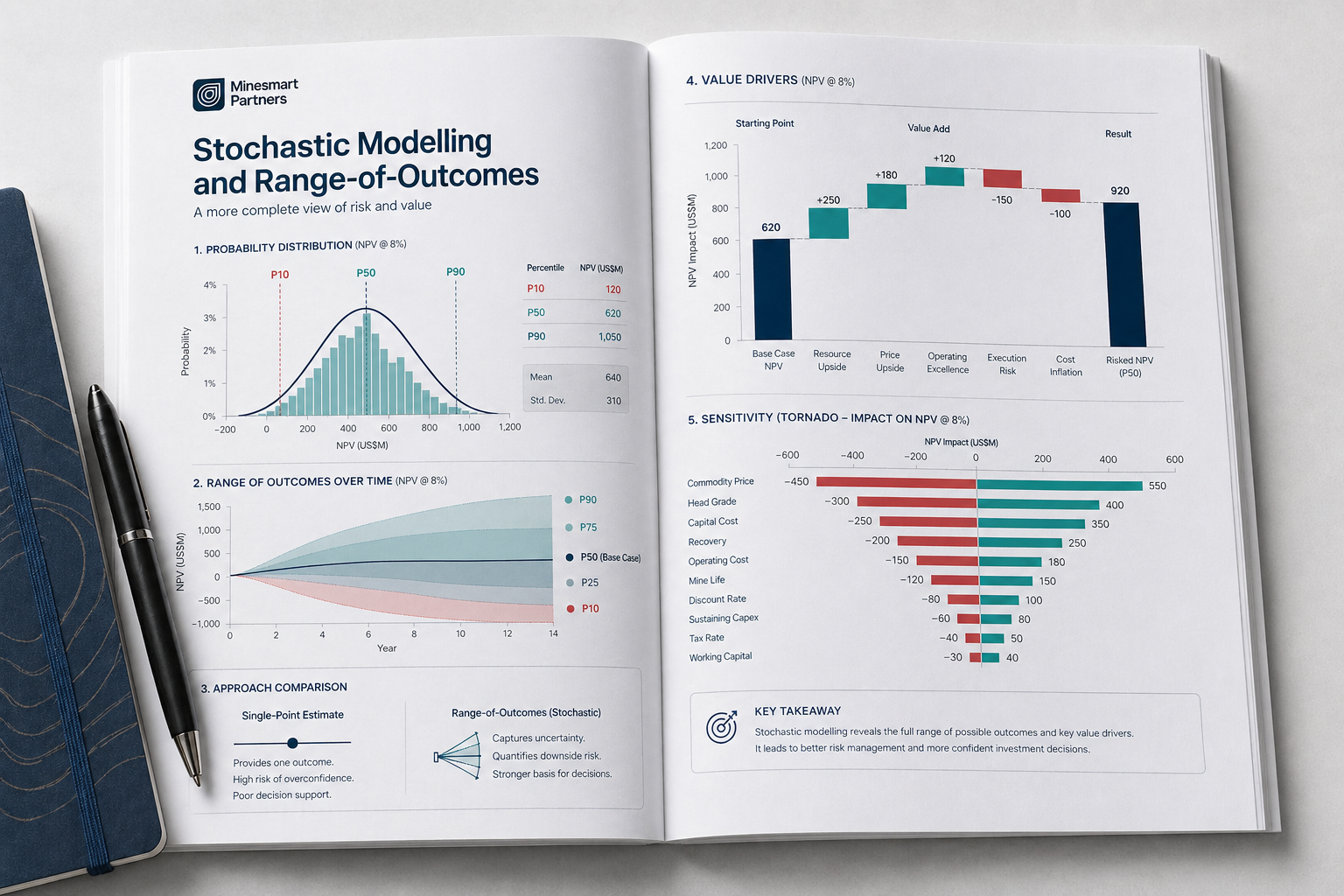

The Bankable Feasibility Study is the definitive technical document for a mining project and it should be. Produced by a qualified person to NI 43-101, JORC, or SAMREC standards, it certifies the reserve base, validates the process design and metallurgical recovery assumptions, confirms the infrastructure concept, and produces a capital cost estimate to AACE Class 3 accuracy. A well-produced BFS gives a lender's independent engineer a solid technical foundation to work from.

The financialmodel accompanying the BFS provides base-case economics across the life of mine. It demonstrates viability under the developer's own assumptions and allows a first-pass view of project returns.

These are real and important contributions. The problem is not what the BFS produces. The problem is what developers assume the BFS covers that it does not.

What the BFS Does Not Cover

The Financial dimension is only partially addressed by the BFS financial model. The developer's model is built to the developer's assumptions. A bank rebuilds it to bank conventions before any credit analysis begins, applying five standard adjustments that are universally applied but almost universally unknown to developers before they experience them for the first time. The resulting divergence — in NPV, IRR, and DSCR — is rarely trivial, and it surfaces at the worst possible moment: during the credit review process, after the mandate approach has already been made.

The Environmental dimension is frequently described in the BFS as work in progress. An ESIA that is ongoing, a permitting process that is active, or a tailings storage facility design that has not been assessed against the Global Industry Standard on Tailings Management are all conditions that a lender's independent environmental and social consultant will identify immediately. Each generates a condition that must be resolved before credit approval.

The Social dimension is the most consistently underestimated by developers and the most frequently cited by lenders as a cause of financing delay. Social licence to operate is not established by an ESIA. It is established through a documented, ongoing, independently verifiable consultation process that demonstrates the informed consent and broad community support of affected communities. Post-Cobre Panama, every Equator Principles lender applies a materially higher level of scrutiny to social licence documentation than was standard five years ago.

The Governance dimension is almost entirely absent from BFS documentation. A developer's beneficial ownership structure, the background of its directors, its anti-bribery and corruption policies, and its exposure to resource nationalism or political risk in the host jurisdiction are assessed by lenders through their own KYC and credit processes. Gaps or red flags in any of these areas will delay or prevent a mandate from being issued regardless of how strong the technical case is.

The Integration Problem

Even when a developer has addressed all five dimensions through separate workstreams — a BFS from SRK, an ESIA from ERM, a financial model from their own team, and legal opinions on title and jurisdiction — the result is three or four documents produced in different vocabularies by firms that have not coordinated their outputs.

A credit committee receives a 350-page NI 43-101, an 80-page Environmental and Social Due Diligence report, and a 50-tab financial model. The environmental risk findings are not reflected in the financial model. The social licence assessment is not connected to the project timeline. The governance risk assessment has never been stress-tested against the DSCR. Nobody has answered the question the credit committee is actually asking: what are the combined financial consequences of the most material risks across all five dimensions?

Three documents. Three vocabularies. Three firms who have never spoken to each other. The credit committee manually reconciles the result — and the gaps it finds become the conditions on your mandate.

The conditions that emerge from a credit committee are not random. They are the predictable consequence of gaps that were visible before the financing process began. A developer who understands what a lender evaluates across all five dimensions, and who addresses those evaluations before approaching the bank, does not receive a list of conditions. They receive a mandate.

What Financing-Ready Looks Like Across All Five Dimensions

A project that is genuinely financing-ready across all five dimensions has four characteristics that go beyond the BFS.

First, the financial model has been rebuilt to bank conventions, with the five standard lender adjustments applied and the DSCR tested under a combined stress scenario. The developer knows exactly where their model diverges from what the bank will produce and has either addressed the divergence or can explain it.

Second, the Environmental dimension is documented in a format that maps directly to Equator Principles EP4 and IFC Performance Standards requirements. The ESIA is complete. The permitting pathway is documented with realistic timeline assumptions. The tailings governance framework has been assessed against GISTM. The closure plan includes a financial provision adequate to cover actual closure costs.

Third, the Social dimension demonstrates documented, ongoing community engagement that goes beyond regulatory compliance to show broad community support. FPIC has been obtained where required. The grievance mechanism is operational. The resettlement plan, where applicable, has been produced to IFC Performance Standard 5.

Fourth, the Governance dimension is transparent and documented. Beneficial ownership is clear. Director backgrounds have been reviewed. The jurisdiction risk profile has been assessed against comparable precedent. The anti-bribery and corruption framework is operational.

None of this is produced by the BFS. All of it is assessable and documentable before the financing process begins. The developers who do this work before approaching a bank do not experience six-month delays. They move faster, with fewer conditions, and with a stronger negotiating position on the terms of the debt.

A lender's credit committee is not looking for reasons to say no. It is looking for the evidence it needs to say yes with confidence. The five dimensions are not obstacles. They are the checklist. The developers who understand the checklist before they walk through the door are the ones who leave with a mandate.

About MinesmartPartners

Minesmart Partners is a specialist mining and criticalminerals advisory firm providing Investment Readiness Assessments,Techno-Economic Modelling, and Integrated Risk Assessments for mining projectsat every stage of development. We occupy the integration layer betweentechnical consultants, ESG specialists, and financial advisors, producing thesingle decision-ready investment case that credit committees, DFI investmentofficers, and equity fund ICs actually need.